Chris Matthews

Chris MatthewsThe issue of health care ought to provide Democrats a smooth limousine ride to the White House. Polling shows that health care is tied for first, along with the economy, as the leading political issue for Americans, and among voters in the upper Midwest swing states likely to decide the election, Donald Trump gets worse marks for his handling of health care than for any other issue.

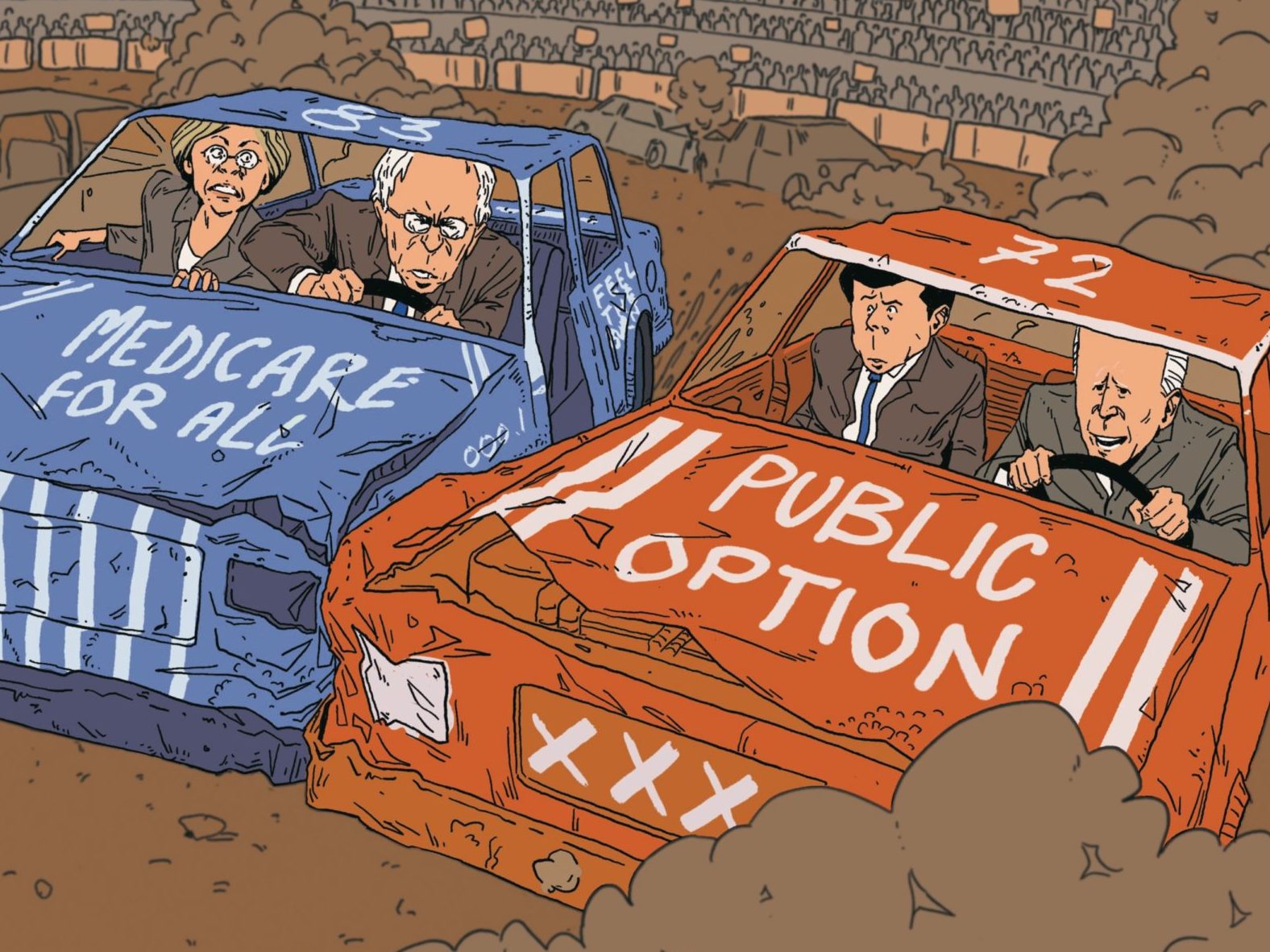

Yet in recent months, health care has been more like a demolition derby—a spectacle in which Democratic candidates bash each other over policy differences in ways that weaken the whole field. This past fall, Elizabeth Warren saw her lead in Iowa and New Hampshire polls collapse after she struggled to explain how she would pay for her single-payer “Medicare for All” plan without raising taxes on the middle class. She has also lost support among likely Democratic primary voters who have become increasingly concerned about polls showing that single-payer would be a political loser in the general election—because, in addition to higher taxes, it would require 157 million Americans to give up the employer-provided health coverage they currently rely on. Similarly, Kamala Harris dropped out of the race in December in part because of her embrace—and then rejection—of Medicare for All.

Joe Biden and Pete Buttigieg have done somewhat better by eschewing single-payer in favor a “public option”—

essentially, building on Obamacare by letting the uninsured and others buy into Medicare or some other government-run health insurance program, with subsidies for those who need them. But these more moderate candidates have not been able to close the deal with the many left-leaning Democratic voters who think America’s flawed health care system needs more fundamental change.

And those voters have a point. America needs change beyond what any extension of Obamacare can offer because Obamacare can’t solve health care’s most pressing and electorally salient issue: rising costs. For the typical medium-income family of four with health insurance, annual health care costs have risen by more than $ 10,000 in the decade since the passage of the Affordable Care Act. Since 2008, deductibles for covered workers have increased eight times as fast as wages. The rising cost of premiums nominally paid by employers is a major reason why so many of us haven’t gotten a raise in decades. Money that might go to increased wages goes instead to cover the cost of unrelenting health care inflation.

Champions of Medicare for All claim that their plan would attack this crisis by giving the government bargaining power to demand lower prices from doctors, hospitals, and drug companies. But even if that’s true in theory, it doesn’t change the fact that Medicare for All is electorally toxic. Its abstract promise of cost control doesn’t overcome voters’ aversion to higher taxes or losing their insurance. Warren and Sanders’s plans’ most-likely outcome isn’t cheaper care. It’s four more years of Donald Trump.

This past fall, Elizabeth Warren saw her lead in Iowa and New Hampshire polls collapse after she struggled to explain how she would pay for her single-payer “Medicare for All” plan without raising taxes on the middle class.

Biden’s and Buttigieg’s plans are far more politically salable, and they claim that the public option, as it grows, could also be used by the government to extract lower prices. That’s also true—for those who choose the public option. But for those who stick with their private insurance (that is, most people in the short and medium term), health care costs will likely skyrocket as hospitals and doctor groups raise prices on employer-provided plans to make up the loss of revenue from the public option. In other words, Democrats might be able to win with the public option in 2020, only to get crushed in 2022 or 2024 as millions of angry voters who were promised health care cost savings wind up experiencing the opposite.

Democrats desperately need an alternative health care plan—one that has broad political appeal and won’t cost the Democrats the next election, yet also gives progressives the structural changes they want. Most important of all, they need a plan for solving the health care cost problem that an overwhelming number of voters say they want addressed.

Fortunately, there is such a plan. With coauthor Paul Hewitt, formerly deputy commissioner for policy at the Social Security Administration and a health economist, I first sketched it out in these pages nearly two years ago. (See “The Case for Single-Price Health Care,” April/May/June 2018.) The core idea is straightforward: Have the federal government mandate that the prices Medicare pays for health care apply to everyone’s health care plan. Call it “Medicare Prices for All.”

If implemented today, it would, in one stroke, dramatically restructure health care markets while dramatically cutting medical costs for most working families, and all without asking a single voter to change providers or health plans, or to pay another dollar in taxes. In fact, if done right, most Americans with employer-provided health care plans would see fatter paychecks. Better yet, if combined with a few other features, it would dramatically reduce administrative costs, eliminate extra charges for “out of network” care and other forms of price discrimination, and put more control over clinical decisions in the hands of doctors.

We know those sound like big promises. It’s legitimate to ask hard questions—like how politically feasible such a plan might be, or whether the promised cost savings would actually materialize.

As it happens, state employees in Montana have implemented a version of Medicare Prices for All for themselves. Since our story was published, the results of that experiment are in. They offer any Democrat who cares to listen the way out of the party’s increasingly acute health care dilemma.

In the fall of 2014, Montana’s 30,000 state employees and their families faced a deep threat. Their health care plan was going broke, with losses on course to reach $ 50 million in just a few years. If this story had played out the way it has for just about everyone else in America with group health insurance, the plan’s members would have faced years of fast-rising premiums, higher deductibles, and an ever-shrinking choice of “in network” doctors. But that’s not the way this story ended.

Mostly that’s because of Marilyn Bartlett. An accountant by training, she had spent the previous 13 years working in the health insurance industry, rising to be the chief financial officer of a company that administered benefits on behalf of group health care plans. But as she neared retirement age, she decided to redirect her inside knowledge of the industry by switching sides. She embarked on an encore career as head of the floundering Montana Benefit Plan, which provides health insurance for Montana state employees, retirees, legislators, and their children, spouses, and survivors.

Bartlett was immediately struck by the crazy prices she saw coming across her desk. Some hospitals in Montana were charging five times what Medicare pays for performing specific medical services, while others charged “merely” double. One hospital, for example, would charge $ 25,000 for a knee replacement, and another would charge $ 115,000. Sometimes a hospital might offer the plan at, say, a 7 percent “discount” on the price of performing a knee operation, but it was a 7 percent discount off a list price plucked out of the air.

Bartlett pressed Cigna, the plan’s administrator at the time she took over, to find out what the hospitals’ real costs were. But Cigna, like other insurance companies and third-party administrators she approached, refused to take on the task. So Bartlett went to the hospitals themselves, demanding to see some cost accounting. But here, too, she hit a brick wall. One hospital told her it didn’t know what its real costs were; the others just refused to share any accounting that might justify their prices, effectively saying to Bartlett and her plan’s members: “These are our prices; take it or leave it.”

Under normal circumstances, people in Bartlett’s position just go along with such ultimatums. As hospitals merge with one another and increasingly combine with doctors’ practices, health care markets in most of America are becoming highly collusive and monopolized. In 90 percent of metro areas, according to measures used by the Federal Trade Commission and Department of Justice in evaluating antitrust cases, hospital markets are highly concentrated, typically dominated by large corporate chains that have bought out smaller community hospitals and in many instances shut them down.

This means that when health care plans go to negotiate with these giants over what prices the hospitals will charge them (and, through premiums and copayments, charge their members), they usually wind up being price takers, not price makers. Hospitals that dominate their local market know that any health care plan doing business in the area must include them in their networks or their members will revolt. And so, like the “Soup Nazi” character on Seinfeld, such hospitals can just say “No soup for you” to any plan that dares to try negotiating for better terms.

This means that for all intents and purposes the prices paid by different health care plans are not determined by open markets balancing supply and demand, but rather by sheer monopolistic power. In the face of such circumstances, insurance companies are busy merging with one another to increase their own monopoly power. Some are buying hospitals themselves. In both cases, plan administrators often just wind up colluding with hospitals and passing the pain down the line, ultimately in the form of increased out-of-pocket costs and a reduced choice of doctors for their customers, who barely have a clue what’s going on.

But what if, Bartlett wondered, she could flip all that?

Her plan was as audacious as it was simple. Going forward, she told the state’s hospitals, the plan would pay all of them at the same rate, and that rate would be fixed at roughly two times what Medicare pays for a procedure. And don’t even think about sending a “surprise” bill to individual patients to make up the difference, Bartlett added. Take the deal or leave it.

Democrats desperately need an alternative health care plan—one that has broad political appeal, yet also gives progressives the structural changes they want.

The hospitals went into battle mode, heavily lobbying the governor and the legislature to shut her down. But Bartlett was in a unique position to withstand the pressure. As she told ProPublica’s Marshall Allen, “I’m 67, so I could give a shit. What are they going to do, fire me? I’m packin’ a Medicare card.”

At first the unions representing state employees objected, fearing that they would wind up losing access to local hospitals that didn’t take the deal. But Bartlett helped to re-channel the unions’ anger by pointing out that it was the hospitals that were threatening their health care, by demanding monopolistic prices and fat financial margins. If hospitals couldn’t get by on two times what Medicare determined was a fair and adequate price, she pointed out, they might need to cut out some waste.

State workers and their unions saw her point and began a letter-writing and public-relations campaign to pressure hospitals that refused the deal. Faced with this and the potential loss of some 30,000 fully insured patients, all of Montana’s hospitals eventually buckled. Soon, Bartlett deployed the same tactics to push down the plan’s prescription-drug bill, and within two years the plan went from projecting a $ 9 million deficit to a more than $ 100 million surplus. And despite their protests, Montana’s hospitals have managed to get by just fine. Across the country, rural hospitals are shutting down. But as of July last year, none in Montana have closed since Bartlett’s plan took effect.

Because of Bartlett’s work, state employees and their families have lower health care costs. But other Montana residents continue to pay some of the highest prices in the country. This means that to lower costs for everyone, the government needs to do what Bartlett did for all Americans, rather than just those who get their insurance through a state-run public plan.

That may seem like a tall task. But it doesn’t require Medicare for All, and therefore isn’t insurmountable. Consider the politics. While Bartlett faced stiff opposition from hospitals, the political forces arrayed against her were not nearly as broad and powerful as those that would have been summoned had she tried to implement anything like a single-payer, Medicare for All–type plan. Deep-blue Vermont, home of Bernie Sanders, tried that in 2011, but couldn’t get it done, due primarily to the daunting political challenge of raising the necessary taxes and broad public resistance to trusting the state government with a monopoly on health insurance. Montana’s approach offers far fewer obstacles. If done on a national scale, it would mean that people who favor the status quo in private health insurance, or who are opposed to new taxes, are not enemies. Indeed, they could join with reformers and demand more reasonable prices for everyone.

Medicare Prices for All has another advantage over Medicare for All: It is relatively simple to enact. Congress would just pass a law pegging all health care prices to some low multiple of what Medicare pays. There’s no need to eliminate private insurance to gain purchasing power over providers. And hospitals could no longer engage in price discrimination, charging different plans (and their members) different prices for the same medical services. It wouldn’t matter whether people lived in a cornered or competitive health care market, whether they were covered by a large or small health care plan, or whether their doctor or nearest hospital was a “preferred provider” or “out of network,” because all providers would get the same prices for the same treatments, just as they do under Medicare. That means no more surprise bills.

The benefits to the more than 100 million Americans who get their coverage through group insurance plans would be dramatic. Let’s do a little back-of-the-envelope calculation. According to Paul Hewitt, from 2010 to 2019, Medicare spending per enrollee rose by 18.5 percent, in line with the Consumer Price Index. Meanwhile, private-sector plans saw their costs rise by 57 percent. One result is a ballooning payment gap: This year Medicare only has to pay about 60 percent as much as private plans do for any given treatment.

The core idea is straightforward: Have the federal government mandate that the prices Medicare pays for health care apply to everyone’s health care plan. Call it “Medicare Prices for All.”

But what if we all got that Medicare discount? Medical costs for working families could easily fall by one-third or more. For those with an employer-sponsored health care plan, this could produce a fatter paycheck. According to Hewitt, a typical middle-class head of household whose compensations this year included $ 14,561 in employer contributions to his or her company’s health care plan, and who paid $ 6,015 in employee contributions, could expect a $ 6,800 to $ 8,200 increase in wages, provided that we required employers to share the savings, as could be done through changes in the laws governing private health care plans.

Pursuing such a reform would, of course, lead to a vicious blowback from the medical-industrial complex. As in Montana, hospitals, especially those charging the highest prices in the most cornered markets, would bring out their big guns. They’d blast television and social media with ads threatening massive hospital closures. In many areas of the country, such as metro Pittsburgh or Cleveland, where large integrated health care systems are among the biggest local employers and sources of campaign contributions, they could certainly count on the support of many state and local officials, who not infrequently sit on their boards. When North Carolina’s state employee health care plan tried to implement a plan similar to Bartlett’s, hospitals proved strong enough to beat back the effort, at least for now.

But as the Montana example suggests, the politics of Medicare Prices for All, while tough, are not impossible. The biggest challenge is overcoming the hospitals’ fearmongering about what will happen if they are forced to live on prices pegged to Medicare. But the idea that hospitals will go broke, or even have to cut back on clinically beneficial spending, is easily rebutted.

There are community hospitals that treat mostly Medicare and Medicaid patients. They learn how to cover their costs by avoiding waste and inefficiency. Meanwhile, hospitals with a greater mix of commercially insured customers are typically flush. Though many of these hospitals have managed to remain classified as “nonprofits” for tax purposes, their excess revenues can often be literally seen in the lavish new buildings and parking lots filled with the luxury cars of overcompensated CEOs, specialists, and administrative staff. The head of the “nonprofit” University of Pittsburgh Medical Center earned $ 8.54 million last year, and 33 other executives each collected more than a million. Data from the AFL-CIO shows that two of the largest for-profit health care systems in America, HCA Healthcare and Tenet, have CEOs earning more relative to their rank-and-file workers than the heads of Bank of America, Morgan Stanley, and Exxon Mobil. Even with all of this bloat at the top, hospitals collectively are earning an 8 percent margin, which, as the health economist Emily Gee of the Center for American Progress points out, is higher than the margins in the pharmacy or insurance industries.

The hospital sector as a whole is so wasteful, overpriced, and bloated with growing legions of administrative workers that it is one of the few areas of American life where standard measures of labor productivity have been declining for decades, even as hospitals deploy more and more expensive and clinically dubious technologies, like proton beam radiation machines. Americans may fret about spending less on health care providers; we trust hospitals and clinics with our lives, and it’s understandable to worry that cutting back their revenue would lead to worse treatment. But study after study shows that America’s excess spending on health care does not improve outcomes. If anything, the opposite is true.

The United States spends more on health care each year than every other country in the developed world but boasts one of its lowest life expectancies. Indeed, America’s life expectancy has been falling since 2014, even as health care spending has gone up. One of the leading causes of this decline—opioid overdoses—is a direct product of uncontrolled and unchecked profit motives in the medical industry. Doctors themselves believe, according to a study published in 2017, that more than a fifth of all medical care is unnecessary. They are right: Over-medication (not just of opioids) and unnecessary surgeries are leading causes of death in the United States.

Meanwhile, the prices Americans have to pay for drugs and medical services are multiples of what people in other nations pay for equally good, if not better, health care. The idea that the U.S. health care system will collapse if it has to live on the same share of GDP as, say, Germany or France, is ludicrous.

So just how would a Medicare Prices for All plan work? The first order of business, of course, is setting Medicare prices. Currently, the Medicare Payment Advisory Commission (MedPAC), a congressional agency, computes what relatively efficient health providers would need to be paid in order to turn a slim profit on their various health services. Then Medicare establishes a base payment rate for different units of service, such as a hospital stay or an operation. Medicare makes adjustments for particular hospitals and other providers based on variables such as their geographic location and the complexity of the conditions they treat.

This process is not without flaws or challenges. Over the years, Medicare has tended to overcompensate specialists and undercompensate primary care doctors and other caregivers—a bias that is replicated in private insurance plans. Moreover, providers treating patients covered under traditional Medicare have the ability to make up for any restraints on their prices by just increasing the volume of their services, such as by performing unnecessary tests and procedures. Medicare is attacking this problem by experimenting with new payment systems tied to patient outcomes that are mandated under the Affordable Care Act.

Going forward, we could further improve pricing by implementing what policy wonks call “all-payer global budgeting.” Under this plan, all insurers, public and private, pay the same prices. But in addition, all hospitals are held to a fixed, global budget, as determined by an independent agency that calculates how much each hospital needs to cover its costs if it runs efficiently. The total amount of revenue the hospital gets to keep stays the same regardless of how many patients it admits or what medical services it performs. As a result, there are no incentives for engaging in unnecessary treatments. Instead, there are incentives to invest in prevention and effective disease management because keeping patients healthy reduces a hospital’s costs but not its revenues.

State employees in Montana now receive a version of Medicare Prices for All. The results of that experiment are in. They offer any Democrat who cares to listen the way out of the party’s increasingly acute health care dilemma.

Maryland has been experimenting with this approach, and so far the results look promising. When a rational, nondiscriminatory pricing system is combined with global budgeting, insurance companies no longer even pay for individual procedures or treatments. Instead, they pay a flat annual rate for the coverage of whole populations. That leaves it up to hospitals, rather than insurance-company bureaucrats, to figure out how to most effectively deploy health care resources in the care of individual patients and local communities.

Notice, too, that moving to such a system should help all health care plans, public and private, as well as health care providers, cut back substantially on overhead costs, just as Medicare for All plans promise to do. Global budgeting eliminates billing. And once price discrimination is eliminated, all sides won’t need so many high-cost executives engaged in secret dealings over who gets to charge what and to whom for this or that procedure. Nor will they need so many executives and consultants involved in mergers and acquisitions designed to increase their bargaining power in price negotiations. Under an all-payer, single-price system, the incentives that have driven wave after wave of consolidation among both providers and insurers largely disappear.

We will still need more aggressive antitrust action in many markets. But just eliminating price discrimination and fixing global budgets would go a long way toward restoring and properly structuring productive competition. Instead of competing over who can grow the biggest fastest and gain the most leverage in pricing and cost shifting, both purchasers and providers of health care can focus on other ways of winning, like who can provide the best customer service and, just maybe, the highest-quality, most cost-effective medicine.